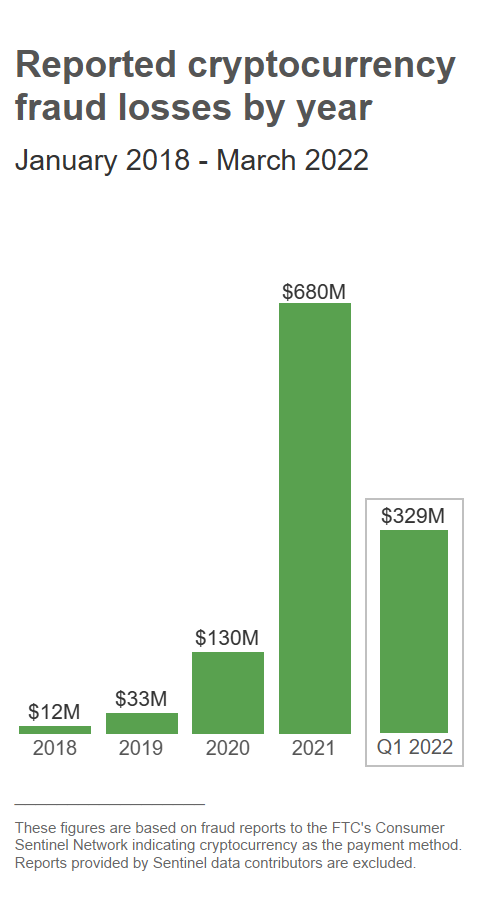

Earlier today the The U.S. Federal Trade Commission put out a report stating that between January ’21 and March ’22 approximately 46,000 Americans have lost more than $1B worth of cryptocurrency to different types of scams.

The figure is a big increase over the previous year when U.S. citizens reported roughly $80M in losses from different types of cryptocurrency scams.

According to the report, even though crypto has not gone “mainstream” as a preferred payment method amongst the broad set of internet users, it has become incredibly attractive as a way to run internet and social media scams:

“Crypto has several features that are attractive to scammers, which may help to explain why the reported losses in 2021 were nearly sixty times what they were in 2018. There’s no bank or other centralized authority to flag suspicious transactions and attempt to stop fraud before it happens. Crypto transfers can’t be reversed – once the money’s gone, there’s no getting it back. And most people are still unfamiliar with how crypto works. These considerations are not unique to crypto transactions, but they all play into the hands of scammers.”

The FTC’s report noted that many of the scams that consumers were led to started as ads, posts, or messages on social media platforms, which promised large returns on crypto investments. The investments would then be made into the scammers crypto wallet.